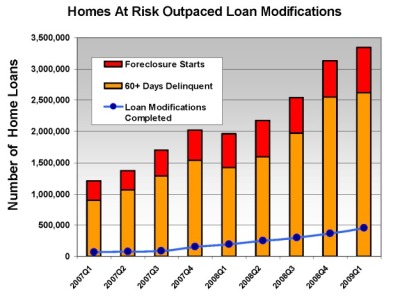

Obama’s mortgage modification plan, HAMP (Home Afforable Modification Program), isn’t working very well. Designed to help prevent foreclosures by incentivizing and giving legal protection to previously indifferent middle-men servicers it isn’t producing anywhere near the number of modifications that were anticipated. Is it likely to work in the future? My guess is no. Let’s discuss some reasons why.

Servicers Gaming the System Over the past few months, more and more stories have come out about servicers finding ways to line their pockets while consumers and investors are getting shortchanged. The one that brought the gaming issue to everyone’s attention is Peter Goodman’s article in the New York Times. Here are my favorite three since then:

Story One, Financial Times:

JPMorgan Chase, one of the first mega banks to champion the national home loan modification effort, has struck a sour chord with some investors over the risk of moral hazard posed by certain loan modifications.

Chase Mortgage, as servicer of several Washington Mutual option ARM securitizations it inherited last year in acquiring WAMU, has in several cases modified borrower loan payments to a rate that essentially equals its unusually high servicing fee, according to an analysis by Debtwire ABS. Simultaneously, Chase is cutting off the cash flow to the trust that owns the mortgage. In some cases, Chase is collecting more than half of a borrower’s monthly payment as its fee.

Story Two, Credit Slips

Countrywide Home Loans (which is now part of Bank of America) has been the subject of proceedings in several bankruptcy courts because of the shoddy recordkeeping behind their claims in bankruptcy cases. Judge Marilyn Shea-Stonum of the U.S. Bankruptcy Court for the Northern District of Ohio recently sanctioned Countrywide for its conduct in these cases…The resulting opinion makes extensive reference to Credit Slips regular blogger Katie Porter and guest blogger Tara Twomey’s excellent Mortgage Study that documented the extent to which bankruptcy claims by mortgage servicers were often erroneous and not supported by evidence. Specifically, the court adopted Porter’s recommendation from a Texas Law Review article that mortgage servicers should disclose the amounts they are owed based on a standard form. Judge Shea-Stonum found that such a requirement would prevent future misconduct by Countrywide.

Mary Kane, Washington Independent

Even as the Obama administration presses the lending industry to get more mortgage loans modified, the practice of forcing borrowers to sign away their legal rights in order to get their loans reworked is a tactic that some servicers just won’t give up on…

In a dramatic confrontation last July, Rep. Barney Frank (D-Mass.), chairman of the House Financial Services Committee, told representatives of Bank of America to get rid of waivers in their agreements. His pronouncement came after Bank of America representatives denied they were using the waivers – and Julia Gordon, senior policy counsel at the Center for Responsible Lending, produced one from her briefcase.

Check out those stories. The first has the servicers set the payment to maximize their fees, and not anything beyond (to make sure very poor and desperate mortgage holders are able to pay each month), making sure their interests are above the lender’s ones. The second one shows that it is very difficult to determine incompetence from maliciousness with the way that servicers are handling their documents on the borrowers end. And the third would be a great piece of classic comedy if it wasn’t so terrible. I bet these guys sleep like babies at night too.

The servicer’s interests are their own – and if they can rent-seek at the expense of the parties at either end, ‘nudging’ them with $1,000 isn’t going to make a big difference.

Redefault Risk There’s another story where the servicers aren’t modifying loans because it isn’t profitable for the lenders. There’s a very influencial Boston Federal Reserve paper by Manuel Adelino, Kristopher Gerardi, and Paul S. Willen titled “Why Don’t Lenders Renegotiate More Home Mortgages? Redefaults, Self-Cures, and Securitization.” They point out that, according to their regressions, redefault risk is very high – the chances that even under a modification there will still be a foreclosures, so why not foreclosure immediately?

I’d recommend Levitin’s critique (Part 1, Part 2), notably that the securitization regression doesn’t control for type of modification, specifically they don’t variable whether or not the modification involved principal reduction, which is probably does for the on-book loans and not for the off-book loans.

But regardless, this is a valid argument as U3 unemployment starts its final march to 10% we are going to see consumers become riskier and riskier, and that will be a problem for modification that will get worse before it gets better.

General Inexperience Servicers were never designed to do this kind of work; they don’t underwrite, and paying them $1,000 isn’t going to give them the experience needed for underwriting. It’s hard work that requires experience and dedication, skills that we don’t have currently. (Isn’t it amazing with the amount of money we’ve put into the real estate finance sector over the past decade we have a giant labor surplus of people who can bundle mortgages into bonds but nobody who can actually underwrite a mortgages well?)

But isn’t it at least possible that as the sophistication of the servicers increase, they’ll become equally good at learning how to game the system? I don’t mean this as a gotcha point, because I think it is the fundamental problem here, and there isn’t any way to break it. The servicers get paid when they have to get involved, and learning the contracts better will give them more reasons to get involved.

It’s been know for several years now that this was a weak spot in the mortgage backed security instruments. In the words of the creator of this instrument, Lewis Ranieri in 2008: ” The problem now with the size of securitization and so many loans are not in the hands of a portfolio lender but in a security where structurally nobody is acting as the fiduciary. And part of our dilemma here is ‘who is going to make the decision on how to restructure around a credible borrower and is anybody paying that person to make that decision?’ … have to cut the gordian knot of the securitization of these loans because otherwise if we keep letting these things go into foreclosure it’s a feedback loop where it will ultimately crush the consumer economy.”

He’s right of course; the people we are trying to ‘nudge’ into acting as the fiduciary are going to be more than happy to rent-seek these instruments while they crush the consumer economy. This ‘gordian knot’ has to be broken, but it’ll need to be done outside the instruments – in the bankruptcy court.