By James Kwak

In 1975, Isaac Ehrlich published an empirical study purporting to show that the death penalty saved lives, since each execution deterred eight murders. The next year, Solicitor General Robert Bork cited this study to the Supreme Court, which upheld the new versions of the death penalty that several states had written following the Court’s 1973 decision nullifying all existing death penalty statutes. Ehrlich’s results, it turned out, depended entirely on a seven-year period in the 1960s. More recently, a number of studies have attempted to show that the death penalty deters murder, leading such notables as Cass Sunstein and Richard Posner to argue for the maintenance of the death penalty.

In 2006, John Donohue and Justin Wolfers wrote a paper essentially demolishing the empirical studies that claimed to justify the death penalty on deterrence grounds. Donohue and Wolfers attempted to replicate the results of those studies and found that they were all fatally infected by some combination of incorrect controls, poorly specified variables, fragile specifications (i.e., if you change the model in minor ways that should make little difference, the results disappear), and dubious instrumental variables. In the end, they found little evidence either that the death penalty reduces or increases murders.

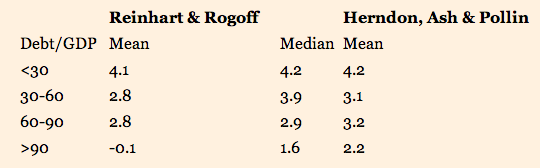

Now the macroeconomic world has its version of the death penalty debate, in the famous paper by Carmen Reinhart and Ken Rogoff, “Growth in a Time of Debt.” Thomas Herndon, Michael Ash, and Robert Pollin released a paper earlier this week in which they tried to replicate Reinhart and Rogoff. They found two spreadsheet errors, a questionable choice about excluding data, and a dubious weighting methodology, which together undermine Reinhart and Rogoff’s most widely-cited claim: that national debt levels above 90 percent of GDP tend to reduce economic growth.

Continue reading “More Bad Excel” →