By James Kwak

James Poterba wrote up a very useful overview of the retirement security challenge in a new NBER white paper. (I think it’s not paywalled, but I’m not sure.) He provides overviews of much of the recent research and data on life expectancies, macroeconomic implications of a changing age structure, income and assets of people at or near retirement, and shifts in types of retirement assets.

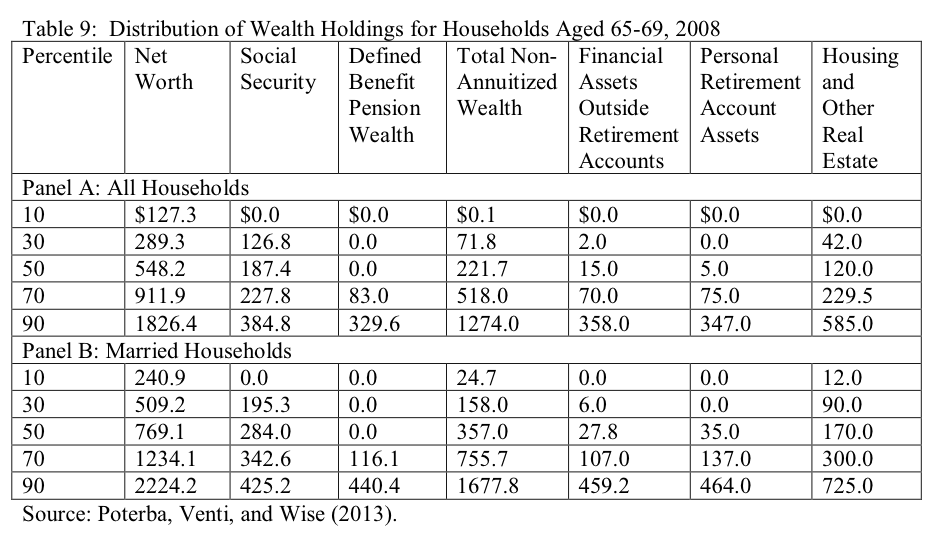

In the past, I’ve used the Federal Reserve’s Survey of Consumer Finances as my source for data about the inadequacy of many households’ retirement savings. Poterba has a new, perhaps even more stark snapshot:

You have to read down the columns, not across the rows. That is, the first row doesn’t give you the financial picture of the 10th-percentile household. Instead, it gives you the net worth of the 10th-percentile household by net worth, the present value of Social Security benefits for the 10th-percentile household by Social Security benefits, and so on.

Still, it’s eye-opening. It says that 50% of households have personal retirement accounts worth $5,000 or less; 50% of households have other financial assets of $15,000 or less; and 50% of households have no defined benefit pensions. 30% of households have total wealth, not counting annuitized pensions, of $72,000 or less. As of late last year, a 65-year-old woman buying a life annuity with a 3% annual escalation clause would get 3.7% of her up-front payment per year (Table 15), so $72,000 in wealth would generate just $2,664 per year—and that’s assuming she finds a way to liquidate her home equity (often the main source of wealth for people in the low-to-medium wealth tiers). And these data are from the 2008 Health and Retirement Survey, so they are only partway down from the housing market peak of late 2006.

These figures might not be so worrying if defined benefit and defined contribution plans turned out to be substitutes for each other—that is, if households without DC plans tended to have DB plans and vice versa. But that doesn’t seem to be the case. First, 26% of households headed by individuals aged 55–64 have no retirement plan at all, and 37% have only one plan (DC, DB, or IRA). Second, it turns out that the more retirement plans you have, the more you tend to have in each one; for example, people who have IRAs, DC plans, and DB plans have higher balances in their DB plans than people who have fewer plans (Table 13).

The overall picture is that the combination of income inequality and a retirement system that largely caters to high-income workers (for example, through tax preferences that disproportionately benefit people in high tax brackets who can afford large retirement contributions) has created vast inequality in retirement preparedness. Poterba does some back-of-the-envelope calculations indicating that people will most likely have to save a lot more than most people are saving today if they want to enjoy decent replacement rates in retirement.

This is true as an arithmetic point, but of course your ability to save depends more than anything else on your income. Absent some form of lifetime income risk sharing (like Social Security), it’s not clear there is a solution for people near the bottom of the income distribution.

The get educated and get one good job belief is a flawed concept. It only works if you are the competitive straight A student now hell bent on abusing your education for money. This leave’s many others at the retirement lurch well before retirement for the lust of money.

The better alternative would have been to have taught more skills and continually increase the efficiency of each skill, from cooking to fixing all the conveniences made for the house. This would have led to more discretionary savings ability for the non straight A student.

It’s the same with the trade jobs too, today you have to do the homework of the producer before buying his product, or fall victim to his many defects.

Tis a strange world he tried to build out there

The result is not surprising, it is hard to save on low incomes! In many taxation systems income from savings are taxed preferentially. Also as noted, retirement savings are preferentially taxed benefiting high income earners.

The other issue in my opinion is the behaviour of savers, in particular discounting long term outcomes highly. Retirement savings are ideally built up over long time horizon. Once a retirement savings gap forms, it is hard to address it in your 50s and 60s.

One solution is mandated contributions such as in Australia where all employers contribute 9.25% of base salary / wage into designated retirement funds. While it would not solve the problem completely, it could partially address the retirement savings gap.

Having great difficulty reading the chart. Could you provided a different explanation of the chart?

The paper is indeed paywalled at the NBER site but at time of writing it can be found on James Poterba’s site at http://economics.mit.edu/faculty/poterba/papers

(Though I’m rather afraid to read it, better get some coffee first)

how exactly does a retiree with dementia ‘manage’ their incomes at retirement?

They mostly don’t dw, and if they do, they have a trusted family member look after their interests. If they make past 90 years, call it a success, less than 80, not so much.

Do they have some more recent data? Like the end of 2012? At the end of 2008 the DJIA was half of what it is now.

elle: I also have more than a little trouble making sense of the chart. It’s not clear to me why Dr Kwak would post data that is aimed at professional economists without a hint as to how to read it. Bit of an insult, really.

One of the best things you can do, for those where it’s possible, and there aren’t serious health issues, is to wait until age 70 to collect Social Security — much higher lifetime inflation-indexed annuity. In fact, if you can wait until 70, and have no debt, including a paid-off, modest-cost condo, you can usually live pretty well just off of that, at least for as long as you can still take care of yourself. It’s a really good base to work for. Usually it’s best to deplete most, or even almost all, other savings to put off taking Social Security.

Boston University economist Lawrence Kotlikoff has details here:

http://www.esplanner.com/case-when-should-i-take-social-security

My brother lost eleven years of 401k savings when the bubble burst in 2007-8. About half of it disappeared overnight due to its investment’s value collapsing, and then when he was laid off (due to the crash) he cashed out the remainder to survive till he could find another job the following year. So he was responsibly saving, had a decent job and income, but a man-made tsunami negated all the money he had put away.

Multiply this sort of thing by millions of Americans, and what role does planning and responsible saving have in most of their lives? The role of designated sucker, apparently.

The more they set aside money, the more that money becomes a target for raiders. Saved money is nothing but a promise of future effort. In a system that doesn’t enforce those promises, the person who receives the effort or money up front (employers and insurance companies, for instance) in exchange for future benefits, can find a thousand ways to renege on their promises without penalty.

We set aside assets in the form of investments, policy payments and so on, purely because we will need them when we become sick and old. But sick people and retirees don’t have the energy to fight back when their promised benefits disappear.

So, where can people safely lodge their savings, assuming they have any? How can they avoid the raiders and the liars? Good question.

@Noni, “…Multiply this sort of thing by millions of Americans, and what role does planning and responsible saving have in most of their lives? The role of designated sucker, apparently…..”

Great post, yes, economic data collection has DELETED from the roll call of USA born and bred souls still on this planet – millions of people with the EXACT same story as your brother – go figure.

I N V A S I O N of privacy is an act of war when it is done by raiders and liars HIRED by NSA and IRS….

Iniquity. Pure iniquity. Although the internet definition of “iniquity” has changed the word’s meaning – it is no longer WILLFUL and pre-meditated harm inflicted on others – ie. “what is torture?”

But, hey, it wasn’t “illegal”….

There’s no point to bending your knee to a “government” that DELETED you from their economic data, is there?

So if a government is not about protecting the individual against force and fraud – LEGAL raiders and liars – it’s not a government.

Mission accomplished.

What’s the next plan for the “history” books….?

Here’s an affordable solution!

southernshoreshomesforsale.com

Here’s the solution:

southernshoreshomesforsale.com