This guest post is contributed by StatsGuy, one of our regular commenters. I invited him to write the post in response to this comment, but regular readers are sure to have read many of his other contributions. There is a lot here, so I recommend making a cup of tea or coffee before starting to read.

In September, the first Baseline Scenario entered the scene with a frightening portrait of the world economy that focused on systemic risk, self-fulfilling speculative credit runs, and a massive liquidity shock that could rapidly travel globally and cause contagion even in places where economic fundamentals were strong.

Baseline identified the Fed’s response to Lehman as a “dramatic and damaging reversal of policy”, and offered major recommendations that focused on four basic efforts: FDIC insurance, a credible US backstop to major institutions, stimulus (combined with recapitalizing banks), and a housing stabilization plan.

Moral hazard was acknowledged, but not given center stage, with the following conclusion: “In a short-term crisis of this nature, moral hazard is not the preeminent concern. But we also agree that, in designing the financial system that emerges from the current situation, we should work from the premise that moral hazard will be important in regulated financial institutions.”

Over time, and as the crisis has passed from an acute to a chronic phase, the focus of Baseline has increasingly shifted toward the problem of “Too Big To Fail”. The arguments behind this narrative are laid out in several places: Big and Small; What Next for Banks; Atlantic Article.

This argument has two components:

Moral hazard: Institutions that are too big to fail create systemic risk; thus the government must rescue them if they make bad bets. This creates asymmetric incentives (one-sided payoffs), which encourage them to make excessively risky bets, thereby encouraging the very systemic risk that regulators are trying to avoid. Governments cannot credibly threaten to let such banks fail because the results (e.g. Lehman) are catastrophic.

The Oligarchs: This argument is best laid out in the Atlantic piece, in a discussion of previous IMF efforts to restore countries to monetary balance:

Typically, these countries are in a desperate economic situation for one simple reason-the powerful elites within them overreached in good times and took too many risks. Emerging-market governments and their private-sector allies commonly form a tight-knit-and, most of the time, genteel-oligarchy, running the country rather like a profit-seeking company in which they are the controlling shareholders.

Although theoretically compelling, most of the evidence for this version of TBTF is indirect:

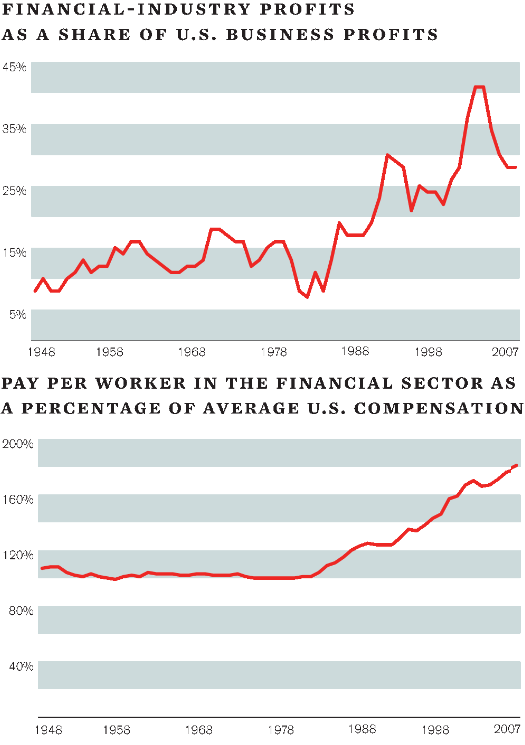

- Higher concentration and profits in the banking industry: (note that the primary source of concentration is clearly M&A activity over 20 years).

- Increasing share of the financial sector in world GDPs and as a percentage of US corporate profits and average wage through 2006.

- The Goldman Sachs mafia (courtesy markets.aurelius).

- Various stories of insiders and whistleblowers who recount specific instances of perverse incentives that encouraged risky behavior.

Along with the explanations underlying Too-Big-To-Fail (TBTF) come certain policy prescriptions that have proven to be very controversial:

a) Take over large insolvent banks (through temporary nationalization or FDIC receivership), sell off performing assets to smaller banks or investors, and break the bank into smaller pieces.

b) If needed, employ anti-trust legislation to break apart healthy mega-banks

c) Build an enduring system that prevents big banks from recreating themselves through M&A (mergers and acquisitions).

Challenges to Too-Big-To-Fail

Timing and Expedience

Is it really imperative to address TBTF first? Attacking banks in the middle of a crisis has high costs (remember Lehman). Would it not be better to wait until the credit/equity markets have fully stabilized and confidence has recovered, and then attack the problem in a quiet orderly manner when banks are not wielding a poison pill over the global economy?

This response to TBTF is rooted in the observation that what began as a financial crisis turned into a global panic, and then morphed into the most intense global recession in 70 years, which almost certainly would have become a depression without aggressive govt. response (capital injections, stimulus, base money expansion). TBTF may have been the trigger, but is not necessarily the most critical step to solving the current global crisis – and solving the financial crisis is critical to addressing multiple other crises (food, water, energy, environment) that were ignored for the past 15 years (and which were recently designated by the National Intelligence Council as threats to national security).

Some TBTF advocates answer that TBTF must be addressed immediately because the window of opportunity may soon shut as the political mood shifts (assuming the economy stabilizes) – see here and here.

In response, the window does not seem that narrow. In a March 26-29 poll, respondents primarily blamed banks and large corporations for the crisis, followed by President Bush (scroll down to see poll). This allocation of blame has been relatively consistent since last October. Obama’s poll numbers seem to have dipped during the February thru March debacle (after Geithner’s disastrous first speech), then recovered as the stock markets staged a rally. Recent in-depth polls showed that the public continued to disapprove of Obama’s handling of bank bailouts even as his overall ratings recovered. The public hates bank bailouts, but not as much as economic decline.

I would therefore argue that the primary order of business is stabilizing the economy. Everyone agrees that attacking TBTF will not be pretty, however – it will take many months to dismantle organizations with trillions of dollars in assets, and the costs of doing this quickly are enormous. (Consider the massive losses suffered in the accelerated AIG unwinds.) In the S&L crisis, the FSLIC and Resolution Trust Corp. did not fully dispose of S&L assets until 1995. The current crisis is worse, and the FDIC and Fed are facing limited organizational capacity. In the meantime, the big banks will not stand idly by.

Rather than attacking TBTF immediately, we may be better served by building a plan that can be implemented after stabilization is achieved. For instance, we might pass anti-lobbying legislation now (something that isn’t likely to cause a collapse in the Dow Jones). Ideally, Team Obama is already building a plan, but if they were, the last thing they would do is announce it. For those who still hope the administration has resisted co-option and corruption in spite of recent revisions of Obama’s anti-lobbying pledge, the Obama Team’s strategy for GM & Chrysler suggests a road forward. The markets may be seeing this as well – as suggested by the recent divergence between bank stocks and CDS prices for bank debt (as SJ and JK note here).

Some TBTF advocates have raised a second justification for attacking TBTF immediately. They worry that the oligarchic bank lobby may sabotage or pervert other reforms, unless the oligarchs are first weakened, and they cite intense lobbying efforts by banks. Reforms such as credit card billing rules seem to be passing at the moment, yet we have no assurance that the Obama Administration will remain able to push such reform through Congress in the future. The rejoinder to these worries is that the Obama Administration’s ability to make future changes will depend on the status of the economy when those changes are sought, which begs the question: how critical is TBTF to securing a recovery?

In its strongest form, the case for attacking TBTF right now states that the economic crisis will not end unless we first deal with TBTF. In other words, TBTF is a root cause of the crisis (though not necessarily the only cause), and any short-term relief we might gain by temporarily accommodating big banks will only backfire in a few years. Although the balance of Baseline’s posts suggests there are many causes, the Atlantic piece does identify the overreaching of elites as the “one simple reason” underlying the economic desperation of developing countries in crisis (which are then compared to the US).

The argument for fixing TBTF immediately to resolve the current crisis thus hinges on the importance of TBTF in causing the crisis. If TBTF is to become one of the dominant narratives behind this crisis, it must contest against other narratives. There are (at least) three groups of narratives that seem to competing with TBTF.

Competing Narratives

Narrative 1: Systemic Risk

A massively leveraged and unregulated financial system is inherently vulnerable to shocks that rapidly get magnified. Perceived (or imagined) risks can create self-fulfilling outcomes, and such risks can be manufactured by large unregulated actors (e.g. hedge funds, which have been immensely profitable for investors over the last 15 years even counting the recent hit).

Moreover, tight coupling of global financial systems and economies causes shocks to transmit rapidly throughout the system, with limited fire-breaks. Contagion, once considered a low risk, can spread rapidly throughout sectors and then throughout the world. IMF report, Figures 1.2 and 1.11 (heat maps)

All of this is worsened by extreme leverage, which has been noted by many scholars (and challenged by some).

Systemic risk was further magnified by the utter elimination of sensible regulation at the behest of free-market ideologues, and indeed the active encouragement of policymakers to engage in risky behavior. Here is a timeline.

In addition, systemic risk is intensified by pro-cyclical policy responses (easing of money in good times, and pro-cyclical factors like mark-to-market in combination with the capital-asset ratio constraints embodied in the Basel Accords).

And finally, systemic risk is massively intensified by the complexity of financial instruments (CDOs, CDSs) which allegedly increase liquidity and volatility (evidence for this is mixed; the VIX volatility index declined through 2006 even as CDO usage intensified), exacerbate systemic linkages (IMF report, Figures 2.1 and 2.6), and decouple the financing/servicing aspects of loans that are usually married together in vertically integrated banks (both creating information barriers, and making loan restructuring more difficult).

In the Systemic Risk narrative, fixing TBTF plays an important role in solving the problem, but not the primary role. The systemic risk narrative suggests that stabilization can be achieved through other mechanisms (reinstating lapsed regulation, lowering overall leverage, reflating the non-debt money supply, better oversight of banks, etc.) Preserving these reforms against political challenges over time is difficult, however, and that is where TBTF becomes important.

Narrative 2: Destruction of the Middle Class

This narrative ascribes the root cause of the crisis to a long-term decline in middle class spending power; the recent financial crisis was merely the straw that broke the camel’s back. The various causes are debated widely, but the end result is clear.

Some versions of this narrative focus on regressive shifts in tax policy since the 1930s, or structural economic shifts that reward higher education, or CEO pay, or the decline in union membership.

Perhaps the most popular version, however, focuses on massive trade imbalances due to unfair trade practices and/or trade with repressive foreign regimes. Unfairly cheap imports have resulted in the hollowing-out of the US economy, loss of real jobs making real things, decrease in labor bargaining power, declines in real median income, increases in US household debt in order to finance stable consumption levels, and a long-term decrease in spending power. The trade deficit data is indisputable: US current account deficit data is here; China specific data is here.

However, the link between international trade and “middle class decline” is heavily disputed (especially by neoliberal economists). Nonetheless, this narrative has begun to win some backing even among free trade elites. For example, Hank Paulson made it part of his mission to convince China to allow the Yuan to appreciate (to address the trade balance) when he became Treasury Secretary, but the world still remained dangerously addicted to US consumption which was largely financed by foreign debt. (45% of world net capital inflows went to the US in 2006)

The “Free-Trade” version of this narrative sometimes focuses on NAFTA, sometimes on China or other countries. It is generally inseparable from a similar narrative that focuses on Greedy (selfish, lazy) US Consumers who spent instead of saved, with the exception that the Free-Trade version blames foreign trade policy and the Greedy US Consumers version blames US consumers who spend more than they earn. Yet the remedy to both is similar – decrease foreign imports, either through dollar devaluation (if you believe foreign economies are manipulating exchange rates and/or the dollar’s reserve currency status caused the dollar to be overvalued) or through trade barriers (if you believe repressive foreign regimes or foreign trade barriers caused the imbalance). Both methods force the US to supply its own consumption. Critics will point to the disastrous results of such policies in the Great Depression (Smoot-Hawley, etc.), particularly when implemented rapidly, globally, and during an economic downturn – so even if trade caused the problem, now might not be the best time to radically reduce imports.

TBTF plays only a limited role in the Middle Class Decline narrative (although the “oligarch” version of TBTF may argue that financial elites engineered the downfall of the middle class to suit their interests). Fixing the problems requires deep structural changes, which may require the eventual political expulsion of special interests (like the oligarchs). But again, this implies that the timing to attack TBTF is a key tactical question.

Narrative 3: Irrational Exuberance (Soft Money, Normal Business Cycle)

The Irrational Exuberance narrative was recently re-popularized by Shiller’s book.

The essence of this narrative suggests that our brains are fundamentally wired to behave irrationally. Behavioral economists are rapidly assembling data to support this assertion. (For example.)

When irrational exuberance takes hold, money becomes cheap as investors expect growth to persist. Consumers and businesses optimistically avail themselves of the cheap credit and increase leverage, until a shock crashes the system and everything reverses. Investors tighten credit, consumers and businesses turn pessimistic, and leverage causes bankruptcies that magnify the problem (just as soft money magnified the boom).

Bank managers have incentives to ride along with the cycle. When everyone else is earning more, bank managers who are “underperforming” are often punished. When the crash comes, managers are often forgiven since everyone else made the same mistakes. Both mass psychology and the competitive environment reinforce this dynamic.

In this narrative, it is hard to argue that bank size matters. Notably, many past financial crisis involved massive numbers of smaller banks, such as the 1930s Great Depression and the 1980s S&L Crisis. Even in the current crisis, many regional banks are also approaching insolvency.

Indeed, we can even cite circumstances in previous history where collusion by large banks has prevented financial crises from become depressions, such as JP Morgan in 1907.

Importantly, there are two distinctive flavors of the Irrational Exuberance narrative – the Austrian version and the Keynesian version. They dramatically differ in their interpretation of government’s role in causing, and solving, economic downturns.

The Austrian School (e.g. Hayek, Schumpeter, Von Mises) contend that bubbles are exacerbated by government activity (and especially by central banks and soft money policies, but also by government spending). According to advocates of this version of the narrative, deregulation did not cause the crisis, it merely happened at the same time. Irrational exuberance can’t be stopped. Bubbles are the problem (made worse, or even caused, by government action), and the “fix” is depression and deflation.

The Keynesians identify the business cycle as a natural outcome of developed economies and capitalist “animal spirits” (alternatively, “spontaneous optimism”), but contend that the system is not self-stabilizing. Notably, business cycles can create credit collapses that cause deflation, and individually virtuous behavior (excess saving) can perpetuate deflation. The system requires an exogenous demand/credit source (like government) to restore equilibrium.

(At this point, I will abuse my role by noting a few interesting data points:

- Contrary to Austrian predictions, the intensity of economic cycles in the US decreased substantially after WWII, when the govt. actively managed the business cycle.

- As Brad DeLong notes, the end of the gold standard marked the beginning of recovery for every major industrial power during the Great Depression (chart on page 4).

- As Paul Samuelson argues, every major US economic expansion died prematurely at the hands of the Fed … This was before Alan Greenspan – a noted fan of Hayek – facilitated and defended the greatest bubble in recent history.)

The Irrational Exuberance narrative is perhaps the least friendly to TBTF. Even the Austrian version identifies TBTF as a problem only because governments have powers they should not have. Remove those powers, and the world-wide depression will hastily fix TBTF. (Notably, this did not happen in the Long Depression of 1873-1879, which was followed by an anemic recovery and the massive inequalities of the Gilded Age). In the Keynesian version of Irrational Exuberance, TBTF is only a problem if the Lords of Finance oppose the aggressive government action that is needed to restore growth.

So Where Does That Leave Us Now?

Your own favored response to the current economic downturn probably depends on which of the narratives above you find most convincing – Systemic Risk, Middle Class Decline, Irrational Exuberance, or Too-Big-To-Fail.

But of course, more than one narrative may be true, and some of these narratives reinforce each other. Combining Systemic Risk and Irrational Exuberance is particularly nasty, for example.

Interestingly, Too-Big-To-Fail synergizes well with the Systemic Risk narrative, and the Oligarchy version of TBTF plays well in the Middle Class Decline narrative. TBTF has a more diminished role in the various Irrational Exumberance narratives.

In the broader context, the Too-Big-To-Fail narrative seems like an upstart next to the other narratives, but it has a few things working in its favor. For one thing, it points the blame at a specific group of people, and Americans really want someone to blame for this crisis. TBTF also taps a populist/anti-elitist sentiment that harkens back to Teddy Roosevelt’s battles against the Robber Barons.

My own objections to TBTF are primarily that TBTF is probably not the dominant cause of the crisis, that attacking TBTF right now could exacerbate the downturn, and that dismantling big banks will require additional measures to address unforeseen complexities (e.g. competing international big banks with lower cost of capital, reduced tools to implement US foreign policy). TBTF is undoubtedly a problem, but is it our most serious and immediate problem?

We are fortunate to have champions like Johnson, Hoenig, and others carrying the banner of Too-Big-To-Fail. Yet while I agree with Baseline Scenario that many other problems in this global crisis require quick action and overwhelming firepower, addressing TBTF requires deliberate and patient action.

I am confident this action can succeed over the long term (should the Obama Administration pursue it) for one primary reason – recent events have widely discredited the dominant paradigm of neoclassical economics. This paradigm, which arguably began with Milton Friedman and was propagated in the public sphere by well-funded think tanks, served as the intellectual artillery that allowed the Oligarchs to shred the laws and regulations that prevented excessive concentration and abuse of financial power. The willingness of respected economic scholars to step forth with new and pragmatic economic ideas is more encouraging than any single change in policy that I could imagine.

By StatsGuy

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Break up the banks. Confine them to only one state, or a tiny national market share (1% or so).

Very well presented. For what it’s worth, I vote ‘all of the above’, with special emphasis on Too Big to Fail. It is worth noting that the business cycle had been pretty well tamed from 1940 or so until recently, an unusually long period in American economic history without a major panic or depression.

Is it a coincidence that Glass-Steagall was repealed towards the end this period? Is it coincidental that Sandy Weill led the charge to do so? Is it random chance that Citigroup is at the heart of the current crisis? Did the efforts at credit default swaps regulation die a natural death, or were they smothered in the cradle by oligarchs?

I’m curious why in the discussion of the polical realities we even bother to cite public opinion. A majority of Americans oppose spending $500 billion a year on defense, an amount equal to the rest of the world combined. But we spend it. A majority of Americans want the U.S. out Iraq. Yet we’re still there. A majority of Americans support single-payer health care, but we don’t have it. And I’d bet the farm we won’t get it, if I had one.

As far as how to address the crisis, we may have already muffed it. Breaking the oligarchy would have been much easier if we had not given it trillions of dollars without much in the way of strings attached. To paraphrase an old song: “I think were turning Japanese.”

StatsGuy —

You are missing one of the major arguments, which is that “Too Big To Fail” is fundamentally unjust.

Taxation, by definition, means using the threat of force to confiscate wealth. That threat is legitimate and just only when it originates from a representative government.

There is a very old English tradition that nobody can take your wealth without your permission, either given directly by you or indirectly by your duly elected representative body. If the “financial elite” really have sufficient control over the state that they can use its to confiscate your wealth whenever they make losing bets, in what sense do you even have representation?

The American Revolution originated from a violation of this principle, and its timing did not much depend on “practical” concerns.

On the other hand, merely as a practical matter, the longer we go down our current path, the more power these “oligarchs” will have and the harder it will be to break that power. Or at least, that is what Prof. Johnson seems to believe, based on precedents he has seen in emerging markets.

Although perhaps you would lump my position in with “populist / anti-elitist sentiment”.

Thia analysis appears to assume that the Icelandic collapse was a one-off.

If we start to see other European economies toppled by their TBTF banks, then the perceived urgency of addressing the issue in the US will quickly increase.

Whoops; should read:

If the “financial elite” really have sufficient control over the state that they can use its power to confiscate your wealth whenever they make losing bets, in what sense do you even have representation?

(a “preview” and/or “edit” feature would sure be handy for these comments)

Why do we have to learn the lessons of the past over and over again?

1. Concentration of power leads to oligarchy, dictatorship or fascism, depending upon historical and local factors. This concentration can be economic, as in ownership of the means of production by the few, or the landed gentry, or the state via proxies (the USSR’s nomenklatura). It doesn’t even require explicit ownership, just functional control.

Economic power leads to political power and/or the reverse. Too big to fail means too big to manage, too big to control and a violation of democratic governance. Such trusts or combines aren’t even good economic engines. They stifle competition and innovation.

2. Moral hazard is a worry without a solution. Those who committed the transgressions are not the ones who will come along later. Did the fate of Mr. Ponzi have any effect on Madoff’s actions? Lessons applied to individuals are not learned by society. What is needed is institutional memory. This is provided by passing laws and regulations which make concrete the lessons of the past. The failure here was to wipe out this institutional memory by repealing and ignoring regulations.

3. Oligarchs work for their own benefit, not society’s. That’s why their existence is incompatible with a democracy. Elizabeth Warren gave a speech on the real destruction of the middle class. The modern necessities (education, health care, transportation) have all increased in cost and consume a bigger part of the family budget. The items quoted by conservatives as a sign of progress, manufactured goods, have gotten cheaper, but are also less of a factor. Here’s a link to her speech, if you’ve got an hour. She did some original research using census data:

We don’t need fancy new economic models to figure out what to do. We need to restore equality of opportunity, create a social safety net similar to other advanced countries, and especially reform the electoral process so that money can’t buy elections and legislators.

A plausible take and breakdown of the narratives. But somehow it doesn’t seem very useful or practical. The commentary did stick out in one way: the mostly implicit way the power theory view of politics and economics was discouraged if not rejected. It seems to me that the very reason these narratives exist is because the well-established process of dealing with insolvent banks was successfully resisted by the banks through their power.

I have not seen one shred of evidence that TBTF is anything other than a fallacy promoted by the banks and associated parties. I suggest TPTA (To Powerful To Allow). The government should let the banks fail and let the FDIC do its work it knows well. Bondholders will loose; common shareholders already lost; and CDS holders won’t make their windfalls.

What we have here is a bunch or rich people losing big bets to a bunch of other rich people. Let them workout the payment problems in bankruptcy court, as usual. Leave the taxpayer out of it.

Ours is not a “financial crisis”, it is an economic crisis. We are experiencing the tipping point of a fall in aggregate demand that leads to a downward spiral in employment and output. The reason is always the same: an unsustainable rise in income concentration. The solution is more progressive taxation, mutual banks, and counter-cyclical fiscal spending as needed.

Why would FDIC receivership not result in payment on CDS?

I think limitations on size is the easiest and most practical regulation available. About 30 banks have been taken over by the FDIC this year, I think.

Totally agree with Lord Tantrum. The smaller banks seem to be doing just fine. Some of the better ones are actually decreasing their loan write offs while still posting a profit…

http://mast-economy.blogspot.com/2009/04/not-all-banks-increased-loan-write-offs.html

My opinion:

Economists are people who don’t know what they’re talking about — and make you feel that it’s your fault….

Just kidding Stats Guy. Thank you for this piece of work. I don’t quite get it all yet, but I’m still in-processing, giving you the benefit of the doubt. My concern is that if we don’t end ‘to big to fail’ now, we may never end it….. we might not have a next-best opportunity. They say the way to eat an elephant is ‘one bite at a time’ —- BUT FRIST, you have to kill the rogue sum’bitch. You don’t kill it by tickling it to death, you pull out the .460 Weatherby and touch it off point-blank between the eyes from 20 paces. Deal with cleaning up the mess later but the deed is done.

BTW – could you disclose your real identity if you’d care to? I was never a fan of the Lone Ranger.

It would. I just meant CDS holders would be in the same boat as other creditors. I specifically had in mind CDS holders who aren’t holding the underlying assets. A full payout is a windfall for them

I think TBTF needs to be address both immediately, in regard to choice financial institutions, and long-term, in regard to all business categories.

I don’t see why addressing TBTF can’t take place now. If GM can be “restructured,” so can the suspect financial institutions. I contend the only reason this restructuring of the TBTFs isn’t being addressed currently is to allow the continued theft of taxpayer money for the benefit of the uber-wealthy.

Capitalism cannot function properly with any business that is TBTF – as that implies a lack of a competitive market. If something is a public necessity and there is a public interest in having the economies of scale available with large (TBTF) institutions, than those institutions should be public (think utilities).

M&As should be the exception, not the rule. Each M&A should have to go through a rigorous evaluation, with the companies carrying the burden to affirmatively demonstrate how such a move will NOT significantly reduce competition, and WILL improve value to consumers.

holders of CDSs have priority treatment during bankruptcy — above depositors. they generally hold collateral, and they are permitted to foreclose on that collateral the minute bankruptcy is declared.

My question: Does too big to fail mean too powerful to regulate? Who is governing whom? And who owns whom?

The global banking system that emerges from this crisis will be one designed around a utilities model, in which bankers receive a guaranteed, modest, fixed-rate of return in exchange for engaging in pro-social behavior.

Something similar to the old Bell System, but updated for a robust 21st century global economy.

Of course, bankers will fight this vigorously, since it will destroy nearly all of their wealth and status. But most assuredly, events will drive this process, not mere banker’s wishes.

Am in the process of digesting this post.

But want to say that the “too-big-to-fail” narrative has always bugged me, for the simple reason is that these large finance companies have in fact failed.

They are bankrupt.

They have no money (except Goldman, apparently, if you read their 2008 annual report) to pay their contractual obligations.

They are loaded up instead with a frightening amount of “toxic assets.” I remain unclear how any smart MBA from any institution (let alone the Ivies) can accumulate such a “moral hazard” on the books.

These financial institutions have failed in ways that have been catastrophic to the economy. Thus the government steps in with a load of dough to ease their pain. (At this point, the pain of most embroiled in the economic crisis – outside of Wall Street – has not been alleviated.)

Wall Street firms getting the bailout are not TBTF – they are too big to let the market have its way with them. Yet the key leaders pay no penalty, bear no burden for their role in the debacle.

I’m not sure that the systemic risk they’ve developed is a moral hazard that must be addressed immediately by flooding all financial firms with billions of dollars, regardless of health, as Paulson determined.

Or if the narrative that the oligarchs have taken over the political process is the more appropriate one for this story.

Who is seeing the most benefit from the actions of the government at this point? And has there been any evidence that the ultimate goal – making loans available for regular businesses and consumers – is now closer to being reached?

Will the bailout ever “trickle down” to the rest of the country?

Nice job Stats Guy,

I think I will read it again. Here are several questions:

About the gold standard, I get it that currency tied to gold is archaic and an impediment to the growth of an economy. At the same time, when Nixon finally took us completely off the gold standard (to make financing the War in Vietnam easier as I understand (misunderstand?) it) we ended up with currency that became in some ways equal to gold. Our ability to essentially print gold, our strong currency, became a burden for manufacturing/exporting and a boon for finance. Favoring finance at the expense of manufacturing was a big step along the path of creating a finance oligarchy and diminishing the middle class.

Second point, TBTF and the oligarchy are inextricably linked because TBTF by definition means that some players are, to use the Animal Farm phrase, ‘more equal than others’.

Last point, i admire the technical ability you and SJ and JK have and your understanding of the complexity of international finance, but at some point, a point I think we have already passed, a complicated and theoretically workable solution becomes practically impossible and a simpler and potentially more destructive solution, at least in the short term, actually works better. This is true in many situations not just because complicated solutions don’t stand up well when they are mixed with politics but also because the unintended consequences and unforeseen problems increase exponentially as the complexity of the solution increases. The beauty of TBTF is more in its simplicity than whether or not it is an entirely accurate description of the cause/cure for the problem.

interesting post, as usual, stats.

my two cents, mostly related to your “irrational exuberance” point.

the crux of why we got to where we are is that

— the united states was able to be fiscally irresponsible for a long period of time with no short term adverse consequences. there was an explosion of public and private debt plus a widening trade deficit. ordinarily these things will correct themselves: an increase in debt will cause borrowing costs to go up; an increased trade deficit will cause the currency to drop in value encouraging exports etc. at the heart of this dynamic was the trade deficit and currency peg with china; essentially china was providing us with vendor financing while trying to build an export sector. basically china wanted dollars, so they sold us stuff cheaply and then loaned us back the dollars so that we could continue buying stuff. safe investments (such as treasuries) had extremely low yields and so investors were pushed into riskier investments.

one note: i would disagree with your statement about hedge funds being long term viable. the graph you display is not asset weighted. in the early years when there were gains, they were much smaller.

another note: the ‘loss of the middle class’ argument goes here. if income (or more properly, assets) were more evenly owned in the US, or if just the rich were in hock to the chinese, then there would be less of a problem.

— demand side housing bubble. from the sidelines (i sold my house in 2003 when i moved across the country and have been renting since) it was amazing to see what people were paying when buying houses. it was a massive self deception. your statement about the oligarchy: “overreached in good times and took too many risks” applies not just to an “oligarchy” but to millions of people in the united states. i know people personally who had no real estate or finance background who bought multiple properties in bubble states at the peak. why did they do this? clearly loose lending standards and tricky loans had something to do with it, but it is also clear to me that people were deceived en masse, mostly by themselves.

a note here: any realistic solution is going to require shutting down or seriously restricting certain modes of credit. when housing switched from a ‘cash flow’ asset to a leveraged asset — through the pervasive use of home equity loans and negative amortization loans — the asset price was bound to go up. this was especially true in a low yield environment (see point above). lending standards that tie the size of allowable mortgage payments to comparable rental payments would be a help here. but also not allowing home equity loans or subprime lending.

— banking deregulation and poor regulation. well, this is mainly what this blog is about so i probably shouldn’t have gone on about the above. however, banks are supposed to be disciplined intermediaries, and the underlying problem is that they facilitated allocation of capital in catastrophically stupid ways, especially in 2006 and 2007. they did this because they had perverse short term incentives, some of which were related to “too big to fail”, but some of which were just “too deluded to succeed”.

however, to me the bigger problem is that we built a banking system with some serious design flaws:

— it responds to shocks not by absorbing the stocks but by creating further internal shocks. case in point is AIG: when AIG was downgraded it failed catastrophically not because of an underlying financial problem but because it was downgraded. one could argue that large banks are in the same situation now — they are hoarding cash because they fear that they will need it as CDS collateral in the event of a downgrade.

— as a related point, derivatives were supposed to help ‘spread out the risk’ but in fact sometimes concentrated the risk (eg AIG) and had their own risks (eg they are marked to market and therefore require liquid markets). when designing these derivatives, nobody asked ‘what if a class of market participants fails to show up’. these risks are systemic, but not specifically related to ‘too big to fail’. you could just as easily see mass insolvency of small players as insolvency of large players.

anyway, i have run out of time and haven’t yet got to the point where my response links up well with your post. i’ll try to continue tomorrow.

Regarding the gold standard, isn’t the USD currently on the OIL standard? If oil were to be sold using some other currency the dollar would be in trouble.

This post is in response to, actually several, made by “TonyForesta” a couple of days ago. I don’t mean to stray from whatever is the current topic, but I doubt if bringing this up here does so as this topic has been continually current on economic blogs for months. If it does, I apologize.

In Mr. TonyForesta’s posts to that thread he passionately advocated revolution, not necessarily violent, or even illegal, but the idea of an organized, concerted struggle by an angry, fed up middle and working class against the “oligarchs” who have been systematically despoiling them for at least a generation.

At one Point Mr. TonyForesta states:

“The predatorclass is so far removed, and so disconnected from the rest of society, and the predator class and their spaniels in the government hold such little regard and respect, and such great disdain for America’s poor and middle class – that they foolishly imagine the poor and middle class will go silently and sheepishly to the flame. They are wildly mistaken. The boiling point is fast approaching. Rage is percolating and seething.”

Now, Mr. TonyForesta, in my experience, I just haven’t seen this percolating, seething rage of which you speak. I live amongst the poor and middle class. I am one of them. When I talk to the people I meet about the financial crisis I don’t find any more actual knowledge about economic affairs than I did when I spoke to my aquaintances before the crisis began. They can parrot back a little bit of current news about the extravagant bonus payouts to AIG execs and shake the their heads. That’s about it.

I sense some unease among people I talk to about the immediate future. Will the plants close? Or can I keep my clients with the layoffs going on? Will I make my retirement? At the same time there’s a vaguely hopeful air that we will get through this as we have gotten through other crises in our lives.

I, myself, have no economic background at all. I pay a mortgage, have an IRA, but I own know stocks or bonds to speak of, and don’t invest, really in any market. For the past several months I have been poring over economics blogs in a not-too-well-focused attempt to educate myself. I have gotten so far in my “study” as to realize that I would need much more background than I currently possess to discuss intelligently or in any depth how we got where we are, or especially, what really should be done about it. (I have a lot of trouble finding useful analysis of that particular sticky point anywhere). The knowledge level I am at now, I can usually safely note that just about anyone I speak with on the “street” about economics, current or otherwise, hasn’t the slightest clue what they’re talking about. But me, I don’t know if we should nationalize the banks, or which ones. Maybe Geitner and assoc. have correctly calculated that any real attempt to nationalize Citi, or another, would precipitate a run the likes of which we have not seen. I don’t know!

Now I know more about the financial crisis than any of my friends do and still have no real clue what needs to be done. Most of them don’t even pretend to care much. They still have their jobs, can pay their mortgage, their car payments, card payments, etc. Things are going to have to get a lot worse for them before they’ll get seriously exercised about the recession/depression. Even then, they’ll have no idea of what or whom to focus their anger on as they haven’t cared to educate themselves.

I don’t wish to be Eeyore. “Nothin’ can be done.” I have learned enough to know that a sea-change is caused in many, if not most instances by a determined and focussed minority. The majority of people eventually move with it (if it does become a “sea-change”). They simply don’t cause it. I think, perhaps, the majority of people are always always fairly passive on larger issues, although they can sometimes be motivated to sacrifice quite a bit if they’re led to it in the right way. If, for example, we Internet bloggers were to find enough energy and spirit to seriously organize our efforts, we might effect change.

I just wish to point out that, in my opinion/experience you can’t count on that “percolating rage” to really give off much heat. That part of what you were talking about sounds inspiring, but doesn’t ring true to my experience, at least.

Regards, jonboinAR

We need to restore equality of opportunity, create a social safety net similar to other advanced countries, and especially reform the electoral process so that money can’t buy elections and legislators.(robertdfineman)

The solution is more progressive taxation, mutual banks, and counter-cyclical fiscal spending as needed. (maldistribution)

The narrative that the oligarchs have taken over the political process is the more appropriate one for this story. (anne)

why in the discussion of the polical realities we even bother to cite public opinion. A majority of Americans oppose spending $500 billion a year on defense, an amount equal to the rest of the world combined. But we spend it. A majority of Americans want the U.S. out Iraq. Yet we’re still there. A majority of Americans support single-payer health care, but we don’t have it. (wildbill)

I am in total agreement with these (and others) viewpoints. The troubling/vexing thing is that they presuppose our system of govt, is, as constituted, unable to bring about these changes. If, as I believe, most of our “representatives” (whom we elected) are in reality acting on behalf of the corporate/financial oligarchs, then how do we (let’s even pretend that most people want these things, partisan affiliations notwithstanding) begin to bring them about, even reforming the electoral process that would be the stepping off point? I don’t mean this to sound defeatist, I have the highest regard for the intellects reflected on this site and wonder what their thoughts are?

Now you have reached the nub of all reform issues – implementation.

Notice that most policy books and essays have a two part structure:

Part 1 – describe the present evils (usually 80% of the document)

Part 2 – state some lofty goals, usually accompanied by the word “should”.

The issues of how to overcome the vested interests are ignored as are any discussions of transition planning.

I’ve tried to deal with this lack in some of my essays, here’s a link to the beginning of one such effort:

http://robertdfeinman.com/society/index.html#plan

Change is hard which is why people don’t address it.

Don’t worry about your lack of economics background. It’s not clear why we are in such a crisis if economics had any real truth to provide.

But, the basics are quite simple: Government Prints money (either on paper or via bytes), Government Gives Money it to Banks, Bankers Take a Percentage of the Money as they dole it out to their Friends who Present Interesting Business Fairy Tales(using economists to justify their outrageous commissions on what amounts to nothing more than a shift of paper from party to antoher), and A Tiny Slice of the Money is Given to 99.9% of the Working Population who are constantly told that working hard is a virtue and the path to riches. Finally, the Government ensures that prices for everything increase every year, so banks can earn enormous profits and 99.9% of the world population needs to work harder and harder to make ends meet and support the bankers.

You see there is no financial crisis. As the government can print as much money as it wants and buy all sorts of garbage for the banks. So there is absolutely no lack of money in this country. The crisis is one of distribution of capital, in the sense that large majority of the money that is printed is not distributed in any meaningful way to produce anything useful for society. Trillions of dollars are given to banks to buy assets that are merely imaginary constructs of a bunch of delusional ex-mathematicians turned bankers and yet people continue to have no electricity in Africa?

But, in the end, it’s all a game. If you can pay your mortgage and support your family, the rest is just intellectual curiosity.

Although I tried to incorporate the many good points raised by commenters on this blog – including you – justice was too big a topic. Nor am I the best suited to offer an opinion, though I have no doubt it is important.

There are a number of excellent comments on the thoughtful post by Stats Guy. I would like to add just one. Capitalism is supposed to “reward” those who take risks and succeed and “punish” those who fail. This concept appeals to a sense of justice – succeed and win; fail and lose.

In this financial crisis, there is a whole new category – those who took no real risks and failed were rewarded – a result which offends any sense of fairness and justice.

Regarding “Dollar = New Gold Standard”, this is the argument that the dollar’s reserve currency status caused the crisis. The dollar’s reserve currency role has allowed us to continue borrowing well past the point that other countries would have been shut out of credit markets, while locking us into policies that defend the dollars abroad so we don’t see a multinational run on our currency.

It has also allowed the US to literally export dollars as a product for other countries to import. Here is what I mean:

The US has partially sustained its trade imbalance by exporting dollars to countries with weak domestic currencies so that these countries can use dollars as their own default currency. This process has a name – dollarization – and some economists have argued it’s a good thing for emerging economies since it provides currency stability (the downside is that dollarized economies literally have to “import” all their money, which is effectively a massive tax).

http://www.imf.org/external/pubs/ft/fandd/2000/03/berg.htm

http://wber.oxfordjournals.org/cgi/content/abstract/lhn012v1

Officially dollarized economies worldwide:

http://en.wikipedia.org/wiki/File:DOLLAR_AND_EURO_IN_THE_WORLD.svg

Also, many emerging economies (e.g. Russia) are unofficially dollarized, and many countries held large reserves of US dollars to defend their own currencies.

That’s a lot of dollars we’ve exported. Many monetarists now focus on the fear that those dollars could “come home to roost” all in one fell swoop if the Fed decides to print money to fight the global downturn. (I suspect this is one of the major fears that caused the Fed to delay Quantitative Easing for so long.)

But those who blame this crisis on cheap imports tell an even more sinister story. The ability to sell dollars (which cost us nothing to make) to other countries has seemed like a great boon that increased living standards (just as neoclassical economists would predict), but in the long term it proved our undoing. The artificially strong dollar made us dependent on imports and gutted our exports – leaving us in the precarious position that when the world finally stops importing dollars we have less to sell them.

Also, there may be a “corrupting” behavioral aspect to “free money”. Leaving aside the “happiness” issue, there is supposedly a study by the Certified Financial Planner Board of Standards showing that 1/3 of lottery winners go bankrupt (though I can’t track it down).

Regarding Dollar = Oil Standard, while it is true that Oil trades in dollars (by international treaty), oil has proved a poor hedge against the falling dollar, and incredibly volatile in dollar terms. For an asset to serve as a basis for money, demand for it needs to be relatively constant relative to the balance of other assets, and it seemed like that was the case for oil. But it turned out that (at least in the short term) demand for oil was more price-elastic than everyone thought. And oil is missing at least one of the key criteria for serving as money – it’s pretty expensive to store.

I think that I agree with what you’ve presented (that stabilizing the financial system and restructuring it are two separate events, and that evaluating the structure of the system needs to take place from a position of objectivity and not in medias res), but it is really difficult to escape the question of justice when the economic sacrifice of merely stabilizing the system is so great.

>>>>If, as I believe, most of our “representatives” (whom we elected) are in reality acting on behalf of the corporate/financial oligarchs, then how do we (let’s even pretend that most people want these things, partisan affiliations notwithstanding) begin to bring them about, even reforming the electoral process that would be the stepping off point? I don’t mean this to sound defeatist, I have the highest regard for the intellects reflected on this site and wonder what their thoughts are?<<<<

Organization, y’all. There has to be a manifesto, of some kind, an analysis of the problem (your Part I), that Part II, the general goals, but then Part III, what do we actually need to do to bridge the chasm? Then there has to be a group of people who are actually willing and determined to put out a fairly enormous amount of effort to create a groundswell. There has to be a party. They have to know what they want to do. I’m thinking (I mean kind of stupidly or vaguely) from my previous post. It’s great to blog ‘n all, and kvetch, but organization is THE key to changing anything.

So, what do you want to do?

rdf, I’ll read your essay.

Oh, dear Lord, you have a bunch of them!

To reiterate what a few posters have already noted above using slightly different wording: what bothers me about the current environment is the hypocrisy. The trouble with leaving these big structures in place is that they represent a fundamental contradiction to the ideals on which our system is supposedly based. In our system, the fundamental narrative runs that we reward success with growth and punish failure with bankruptcy. These organizations have now become big enough (and correspondingly powerful enough) that they are being rewarded (with taxpayer money) for failure. This may be a simple restatement of the concept of moral hazard, but the very people who are now arguing that they are TBTF are the exact same people who were the loudest proponents of “let the weak fail” before they themselves failed. Hypocrisy pisses me off. On a more practical note, however, how do we expect to rebuild a functional economy when the people leading it have lost the lifeblood of all economic activity: trust? Without that component in place, I don’t see much growth. We need a system in which the various members trust and have faith in each other. That means breaking up the current power group and throwing the discredited leadership out.

Allow me to clarify: I was trying to argue that the basis of value in the case of oil is not the oil proper, rather the treaty agreeing to trade oil in dollars. The treaty is the asset not the oil.

Well said, SG, but I think that the problem isn’t one or two of these, but all of them. And looking at the results of this mess, I will throw out the idea that these did not operate as a sum, but rather as multipliers or *gulp* exponents.

Just think about it, from this engineer’s perspective:

Using the business cycle as a base, cycle is on upswing circa 1986.

Money made during boom allows political access to lighten regulation and oversight, increasing systemic risk, moral hazard, and reaping short term profit which translates to greater political power.

Real wages stagnate (cycle?), but credit is easy and encouraged to help make up for lack of wage growth while expectations for it exist, increasing systemic risk, moral hazard, and reaping short term profits and additional political power.

Cycle busts, exposing all of the problems we have seen, but the cycle doesn’t work for the (now) oligarchs since they have accumulated so much political power and personal fortunes.

These things are all part of the system. One aspect you omitted is unlawful activity such as fraud, collusion, racketeering, etc. Fraud, from all aspects of the operation, played a huge part in building the credit bubble. This poses a systemic risk, not necessarily to the economy but to the Rule of Law and constitutes a direct threat to the governance of the United States. How so? If you are prosecuting (for example) securities fraud against the top level of management at one of the TBTF banks. The prosecutor would have to build a better than airtight case in both substance and procedure to overcome the unlimited resources of the defendant. The prosecutor’s office would face political pressure to call off the investigation, including budget cuts to the investigating department (e.g. EPA under G.W. Bush). Now I’m an engineer, not a lawyer, but this is the effect of Oligarchy on a society and the biggest reason why, for political reasons and not economic ones, that the TBTF institutions need to be disintegrated regardless of the economic consequences. This is a political (and arguably existential) disease in the US, the worst symptom being the financial/economic crisis.

I’ll assume everyone here is familiar with Mussolini’s flavor of fascism, so I’ll let all y’all decide whether or not the US is there yet…

Very nice job, Statsguy. Thoughtful and organized thinking about the root causes of the problem and possible solutions. I’ll go back through the article and read the material you’ve linked to.

Question 1: If we don’t tackle TBTF banks now, how can we keep these oligarchs from continuing to suck us dry in piecemeal fashion?

Question 2: If they continue to suck us dry with bailout after bailout (because we can’t let them fail), how do we solve the overall problem?

These are real questions, not rhetorical ones. If you care to reply, I’d appreciate the continuing dialog.

Great post StatsGuy, a very good read, and easy for us non-economists!

I’ve been reading this blog since it’s inception, and I was always impressed with your comments.

What I’ve taken away from your post, is basically TBTF needs to be taken in context with other factors that caused this mess, and that it may not be the most important issue to address, and might even be harmful if pursued right now. This seems to be the biggest difference in your and SJ’s priorities for the economic recovery.

But if we can agree that TBTF is a problem that should be fixed, how important is the “window” issue?

If we take a historical perspective, does anyone know of any other time besides economic upheaval, or perhaps business scandal (think Enron) when major financial reforms were possible? Especially when compared to how powerful politically the financial sector is right now? Those answers might give us a better idea of how long this window will be open for, and how important it really is to push against TBTF now.

Thank you and I look forward to more posts StatsGuy!

With regards to the window of opportunity issue, I think that it can remain open longer than many people realize. The fear is that the Obama administration will lose its nerve once (if!) the economy turns around and not want to risk political capital on fixing systemic risk down the road. My feeling is that if the analysis from the TBTF crowd continues to be compelling at that time, the administration will eventually confron the oligarchs, but it won’t be straightforward.

The Obama administration typically handles political problems with a rope-a-dope strategy. Look at how the torture memos came out. They release this stuff and say at the same time they won’t prosecute (but they will enforce the law). Of course everybody is appalled and demands prosecutions on the grounds that the torture violated the law, and later on after congress insists on truth commissions and everybody has grown sick of the nasty details (and maybe after a mid-term has strengthened Dem control), Holder will start to bring charges after all.

I expect a similar pattern in confronting bank oligarchs. Obama knows full well that only a tiny minority of economists and informed bloggers and their readers have any sense of what is really going on. Popular as he may be, he simply doesn’t have the mandate of an FDR who entered office with massive unemployment, poverty, civic ruin, etc already affecting the lives of millions. The tangible effects of the Great Depression drove home to most Americans the need to give him wide latitude in addressing the crisis. Severe as the current crisis may be, and even if it has the potential to cause hardships similar to the GD, it has not done so yet. Even unemployed americans are still managing to get by so far.

I think that ultimately, so long as you believe that Obama is more or less incorruptible (he will put what he sees as the countries interests above his own), then the window will not close. With his presidency only three months old, I think it is reasonable that those who support him give him the benefit of the doubt on this issue and hope that he is delaying action against the oligarchs so that he can fight them at the greatest advantage.

Oddly my post is gone, but the point jonboinAr is that these energies are moving anyway. The predatorclass is acting in unhealthy ways, that endanger the herd, the pack, the tribe, the pride, et al – and – for the sake of our children – we must all work toward ways that promote good health in our societies and economies.

The oldworldways are corrupt, venal, merciless, and toxic, – it is time for a new paradigm, and new awakening and real equality and equanimity in the markets and our societies. If not, – we burn – “…in the rockets red glare, their bombs bursting in air.”

A thousand pardons, I misposted this comment on the wrong thread, and post it here, where it was intended with a few edits.

(Outstanding commentary StatsGuy. While I still hold (that) the underlying dynamics reach into moral or ethical realms and how we exactly define ourselve as a nation and a people, (I apprecaite your temperance and diligent research.

Are we wanton greedmongers, – obdurate, heartless, ruthless, swindlers and theives, – PONZI scheme operators – willing to stomp on, and suck off the blood of poor and middle class Americans to feed the superrich, the predatorclass, – or are we a nation that honors the Constitution, the rule of law, the core principles that formally defined America?

It is a profound decision (that) will shape what we are, and will become “goingforward” (as a nation).

What you have successfully acomplished though, is to inspire people from our lowly perches to re-examine the Obama approach through the lens of preventing, or minimizing economic calamity.

The clock is ticking. Obama owns a vast well of goodwill. Many of us are distrubed by the seeming overt favoritism and hyper extraordinary government largess towards the banks, and Goldman Sach particularly, – but we are willing to afford the Obama government a bit more time to sort through this horrorshow and calamitous economic crisis we all recognize Obama inherited from the bushgov.

Let us hope that Obama’s methodical approach truly does have the best interests of the American people, and not Goldman Sachs, or the predatorclass swindlers and thieves on Wall Street at heart.

Yet there is no such thing as excusing or cloaking crimes. If these pernicious) and perfidious policies exist, – then effectively – there is no law. And in a world where there is no law, – there is no law for anyone predators.

Your posts are always instructive, StatsGuy.

“The essence of this narrative suggests that our brains are fundamentally wired to behave irrationally. Behavioral economists are rapidly assembling data to support this assertion.”

It would be better to understand that our brain is not “fundamentally wired” to behave either Rationally or Irrationally, in particular. We make those terms up to help organize observations. Maybe the rapidity and complexity of technological development over the last 200 years led economists to believe they were studying a “system” that could be measured and manipulated by following mechanistic models and laws, once

you had figured out what they were. But economics is nothing more or less than social behavior, and social behavior is too complicated to manipulate purposefully, given our present knowledge of it. The best we can do is to regulate it when we recognize a need and see a possible regulation.

TBTF is a recognition of a need to regulate. The legislatures that allowed the assembly of these behemoths, and the bankers who assembled them, as they moved into the position of oligarchs, were doing what people do. People will do it again the next time circumstances allow. The only defense the public has against those circumstances occurring is regulation. The belief that there is a system, an economy, that can be

influenced by the right combination of confidence, incentive, rationality, self-regulation, etc., etc., is a red herring. Regulation can be crude and even destructive, but it is all we have to protect the many from the few. We need to use it now and pick up whatever pieces are left afterward, fit them together however we can and see what happens.

Of course, this is easy to say from a position of comfortable retirement, but still, I don’t see any alternative. And I’ve been looking for a long time.

Stats guy, you wouldn’t be Eric Friedman would you? Possibly Allasdair Breach?

“This paradigm, which arguably began with Milton Friedman and was propagated in the public sphere by well-funded think tanks, served as the intellectual artillery that allowed the Oligarchs to shred the laws and regulations that prevented excessive concentration and abuse of financial power”

Well we figured out what Friedman and the think tanks were up to quite a long time ago.

“more than one narrative may be true”

How about if all are true? But it doesn’t matter? If you’re truly clutching about for an immediate action plan, maybe you shouldn’t be? This all feels very large and quite unavoidable. After we blew off our synthetic financial/real estate economy we saw that we really don’t have much left. Little manufacturing. Our big manufacturers, the auto industry, are dying painful deaths currently. We have automated ourselves and created fantastic efficiencies that obviate the need for a large labour force. In the US, we are turning out barely literate and illiterate students who can hardly be expected to assume roles in a knowledge industry. Icelanders are being airlifted to central Manitoba and will be absorbed into the local economies, but where will the Irish go? The Americans? Eastern Europeans? Asians? Big things are afoot, Stats Guy, bigger than you deal with here, but you probably know that.

“In September, the first Baseline Scenario entered the scene with a frightening portrait of the world economy”

Quite so. Fear, fear, fear. The balloon inflated with greed, and it is deflating with fear.

The phrase “too big to fail” is applied by tortured analogy to non-FDIC-insured financial institutions, and the expression doesn’t mean what politicians like to pretend that it means. It means that the deposit liabilities of a systemically important bank are not subject to deposit insurance limits. That’s all it means. It doesn’t mean the bank can’t be taken into custodianship or receivership. It doesn’t mean that every creditor will be made whole. It doesn’t mean that shareholders are protected. It means that a sudden huge loss of uninsured _business_ deposits and _correspondent bank deposits_ won’t happen. The law in this matter has absolutely nothing to do with Bear Stearns or Lehmann, and regulators have acted outside the letter and intent of the law in order to protect unsecured creditors, shareholders, and counterparties.

No narrative is correct, all narratives are correct…

Reality is a gigantic non-linear aggregator of causes. It tosses all the narratives we’ve discussed and some we haven’t into a pan. We get an outcome, a souffle, and the narratives are only true insofar as they help us to think about which ingredient was the biggest.

IMO, the use of narratives is only in persuading others to pursue a policy that you decided was correct by use of some rigorous analytic method.

Most intellectually sophisticated post I have read in ages – bravo.

Regarding “narrative no. 2,” our enormous trade deficit is rightly of growing concern to Americans. Since leading the global drive toward trade liberalization by signing the Global Agreement on Tariffs and Trade in 1947, America has been transformed from the wealthiest nation on earth – its preeminent industrial power – into a skid row bum, literally begging the rest of the world for cash to keep us afloat. It’s a disgusting spectacle. Our cumulative trade deficit since 1976, financed by a sell-off of American assets, exceeds $9.2 trillion. What will happen when those assets are depleted? Today’s recession is the answer.

Why? The American work force is the most productive on earth. Our product quality, though it may have fallen short at one time, is now on a par with the Japanese. Our workers have labored tirelessly to improve our competitiveness. Yet our deficit continues to grow. Our median wages and net worth have declined for decades. Our debt has soared.

Clearly, there is something amiss with “free trade.” The concept of free trade is rooted in Ricardo’s principle of comparative advantage. In 1817 Ricardo hypothesized that every nation benefits when it trades what it makes best for products made best by other nations. On the surface, it seems to make sense. But is it possible that this theory is flawed in some way? Is there something that Ricardo didn’t consider?

At this point, I should introduce myself. I am author of a book titled “Five Short Blasts: A New Economic Theory Exposes The Fatal Flaw in Globalization and Its Consequences for America.” My theory is that, as population density rises beyond some optimum level, per capita consumption begins to decline. This occurs because, as people are forced to crowd together and conserve space, it becomes ever more impractical to own many products. Falling per capita consumption, in the face of rising productivity (per capita output, which always rises), inevitably yields rising unemployment and poverty.

This theory has huge ramifications for U.S. policy toward population management (especially immigration policy) and trade. The implications for population policy may be obvious, but why trade? It’s because these effects of an excessive population density – rising unemployment and poverty – are actually imported when we attempt to engage in free trade in manufactured goods with a nation that is much more densely populated. Our economies combine. The work of manufacturing is spread evenly across the combined labor force. But, while the more densely populated nation gets free access to a healthy market, all we get in return is access to a market emaciated by over-crowding and low per capita consumption. The result is an automatic, irreversible trade deficit and loss of jobs, tantamount to economic suicide.

One need look no further than the U.S.’s trade data for proof of this effect. Using 2006 data, an in-depth analysis reveals that, of our top twenty per capita trade deficits in manufactured goods (the trade deficit divided by the population of the country in question), eighteen are with nations much more densely populated than our own. Even more revealing, if the nations of the world are divided equally around the median population density, the U.S. had a trade surplus in manufactured goods of $17 billion with the half of nations below the median population density. With the half above the median, we had a $480 billion deficit!

Our trade deficit with China is getting all of the attention these days. But, when expressed in per capita terms, our deficit with China in manufactured goods is rather unremarkable – nineteenth on the list. Our per capita deficit with other nations such as Japan, Germany, Mexico, Korea and others (all much more densely populated than the U.S.) is worse. My point is not that our deficit with China isn’t a problem, but rather that it’s exactly what we should have expected when we suddenly applied a trade policy that was a proven failure around the world to a country with one fifth of the world’s population.

Ricardo’s principle of comparative advantage is overly simplistic and flawed because it does not take into consideration this population density effect and what happens when two nations grossly disparate in population density attempt to trade freely in manufactured goods. While free trade in natural resources and free trade in manufactured goods between nations of roughly equal population density is indeed beneficial, just as Ricardo predicts, it’s a sure-fire loser when attempting to trade freely in manufactured goods with a nation with an excessive population density.

If you‘re interested in learning more about this important new economic theory, then I invite you to visit either of my web sites at OpenWindowPublishingCo.com or PeteMurphy.wordpress.com where you can read the preface, join in the blog discussion and, of course, buy the book if you like. (It’s also available at Amazon.com.)

Please forgive me for the somewhat spammish nature of the previous paragraph, but I don’t know how else to inject this new theory into the debate about trade without drawing attention to the book that explains the theory.

Pete Murphy

Author, “Five Short Blasts”

I agree that all of the above mentioned narratives played a role. I also agree that theoretically TBTF can be set aside for reform at a later date; however our financial resources and international credit worthiness are limited. TBTF is an immediate problem when TBTF believes that they don’t have any problems and that their failing assets are fine. We can not allow TBTF to ignore its own problems, it only delays and increases the final costs. If TBTF was cooperative in fixing the problem we could wait until later to correct it, however that cooperation is not happening.

I am going to refrain from posting my specific ideas on this thread, because it feels like an abuse of privilege. But I will join the discussion in future threads.

Ah, I see.

“I am confident this action can succeed over the long term (should the Obama Administration pursue it)”

I am not confident, and the Obama dministration will not.

James laid out the reasons pretty well, I think of it as the economic version of Wilson’s concept of “Evolutionary Stable Strategies”. Call it “Democratically Stable Regulation”, i.e. laws and regulations that are subject only to educated majority vote and not subject to minority lobbying financed by the circumvention and abolishment of the very same regulations they are targetting. From that starting point, it follows that the majority has to be wealthy enough and educated enough, that lobbying has to be prohibited, and that financial institutions (as well as any other entity Too-Big-For-Democracy) have to be broken up. But even if Democratically Stable Regulation can be found to prevent establishment of Too-Big-For-Democracy structures, our first problem is that these structures already exist, and that the demoractic process is already rendered dysfunctional. Hence, no administration – especially not an Obama administration that keps Bernanke despite Bofa-Merrill, elected Geithner despite his IMF tenure on Indonesia and his performance as Wall Street’s Fed during the last 5 years, and selected Summers despite aiding and abetting the deregulation rampage at the close of Clinton’s reign that set the stage for the terminal escalation of the bubble cascade.

History implies that societies that lost their ability to reform are never reformed, they fall apart – often violently. I do not see a compelling case for complancency, even on the side of the looters and criminals.

A very thoughtful and well-constructed discussion.

However, here’s a reason why TBTF needs to be at the top of the list which was not covered, and which in my view trumps the well-made arguments above:

This is not a purely economic crisis, it is also political. There’s a lot of discussion out there as to whether the financial system is struggling with liquidity or solvency; but these are simply two competing views of the same economic symptoms.

What’s really at the bottom of the crisis is the credibility of the economic and political leaders who have brought us to this point. Stat’s Guy’s narratives are each compelling and valid, and I agree with them all.

However, the existence of the first two of SG’s narrative was driven by political decisions made as a result of the lobbying efforts of the leaders of the TBTF institutions, and more importantly, the public is well aware of this fact: we all know we’ve been screwed, we know who’s been screwing us, and we will not believe in any solution that does not prominently include holding these institutions to account.

Tackling TBTF first has the virtue of initiating the reestablishment of the credibility of the political leadership, by demonstrating the supremacy of the electorate’s political will over the nation’s economic resources.

If the credibility of the political leadership is not effectively reestablished either before or concurrent with a return to economic stability, a significant portion of the public will remain suspicious and hostile to the ruling economic and political elites.

All this being said, I agree with SG that it is important not to assume that tackling TBTF will solve the crisis – he is right that TBTF was the trigger and is not responsible for the larger, underlying structural imbalances in the economy.

Those imbalances are the result of decades of political and economic decisions made by leaders who feared to tell the public the truth because it could have resulted in losing power.

More than anything else, the public wants to be able to trust their leaders; and more than anything else right now, they are aware that those who led us into this cannot be trusted to lead us back out. They simply need to be identified and removed from power.

One of the problems is we see what we look for. It’s an old story but still true.

So for my pennyworth I put forward another thought. All the above explanations presume the ‘rule of law’ applies inn the US and UK. But it doesn’t.

People lied on mortgage applications, the staff at mortgage providers knew many were lying yet processed them anyway, lawyers and mathmaticians packaged up these ‘liar loans’ and sold them on as AAA knowing they were nothing of the sort. All of it was just straight forward crime.

Multi-million dollar contracts were made that didn’t benefit the firms, they were made for the bonus’ the participants recieved. Thats fraud.

In the UK house prices rose 15-25%pa for 10 years while wages rose just 2-4%pa. The govt knew it wasn’t sustainable but didn’t care because the ‘feel good’ factor helped it get re-elected, and to strengthen the bubble refused to act to increase the building of family homes despite numerous reports. Granted not dishonest, but it was dishonourable.

The demise of the ‘rule of law’ has seen the development of a culture dominated by dishonourable and dishonest behaviour in the UK and US. The result is widespread criminality. It’s not just the millions of frauds varying from £100s,000 to 100s of millions, there are the tennants of publically funded homes letting them out at private rents. Corruption in housing and planning departments. It goes on and on.

Yet our governments are still unwilling to apply ‘the rule of law’.

A fair chunk of the troublesome mortgages and loans don’t exist, they were frauds. Likewise many contracts done for the bonus. We need to unpick the lot, prosecute the crooks and try and cope with the fall out.